Dealing with debt collection can feel like an overwhelming battle, leaving many consumers stressed, confused, and unsure of where to turn next. The Consumer Financial Protection Bureau (CFPB) reported an increase in consumer complaints about debt collection in 2024, highlighting the prevalence of this issue.

One effective tool to address and potentially halt unwanted debt collection practices is the Fair Debt Collection Practices Act (FDCPA) Demand Letter. This legal document allows customers to stand up for their rights, ask for debt verification, and seek cessation of harassing communications.

In this article, we will explore the purpose of the FDCPA demand letter, outline its key components, and provide a step-by-step approach to crafting one.

A Fair Debt Collection Practices Act Demand Letter is a formal notice sent to a debt collector asserting your rights under the FDCPA. Its primary purposes are to:

To safeguard your rights throughout the process, sending this letter may suspend collection efforts until the debt collector produces the needed verification. Let's look into when and why you should use the FDCPA demand letter.

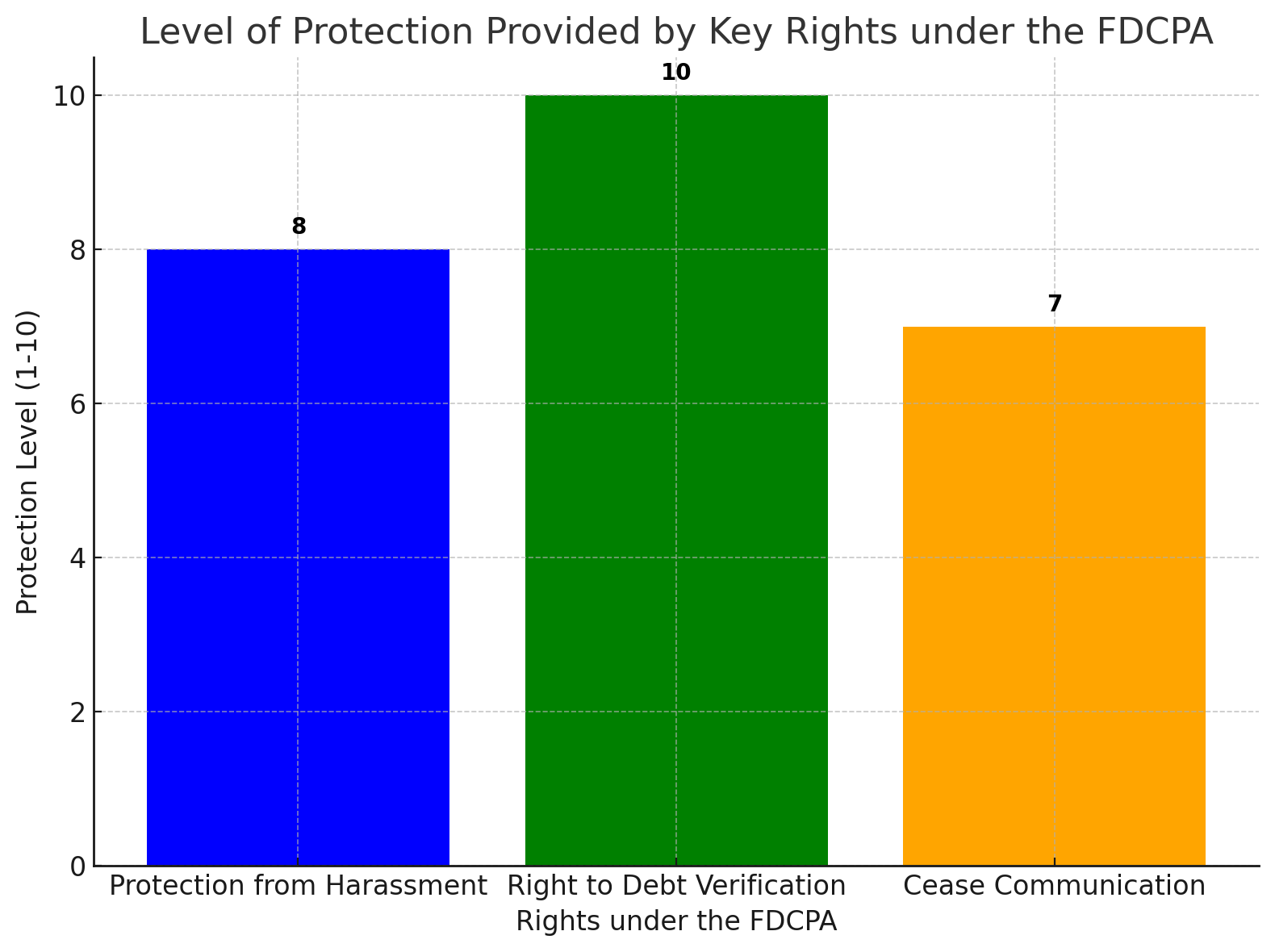

When dealing with debt collectors, being aware of your FDCPA rights is important. These key protections ensure that you receive fair treatment and are protected from unethical behavior:

The above chart displays the level of protection provided by the three key rights under the FDCPA. The Right to Debt Verification offers the highest level of protection, ensuring that debt collectors must provide proof of the debt.

These rights are in place to prevent aggressive and unjust collection methods while ensuring you're treated with dignity.

According to the CFPB's 2024 report, attempts to collect unpaid debts accounted for more than 53% of debt collection complaints, highlighting the need to understand and defend your rights.

Keeping these protections in mind, let's explore the key components your FDCPA demand letter must contain to succeed.

To be effective, your FDCPA demand letter must include key components communicating your rights and requests. You may make sure the letter is comprehensive and legitimate by including these components:

The above flowchart illustrates the steps to draft an FDCPA demand letter. Each step is clearly defined, leading from the Identification and Debt Details to setting a Compliance Deadline.

By including these key components, you can ensure that your letter will properly address your rights and be legally effective. Now that we know what should go into the letter, let's look at the practical steps for drafting and sending it properly.

Although completing the FDCPA demand letter may seem overwhelming, you can take a few easy steps to ensure your letter is understandable, professional, and legally valid. Here's how to correctly fill it out:

Include Your Name and Address: At the beginning of the letter, make sure your name, address, and other personal information are prominently displayed. By doing this, the debt collector will better identify you and the debt in question.

By following these steps, you can ensure your demand letter is transparent, professional, and compliant with the law. Let's look at a sample demand letter to see how these elements come together in practice.

Now that you have your demand letter ready, it's time to send it to the collection agency. Let's explore the proper steps for mailing and tracking your letter.

Once you've crafted the perfect demand letter, it's time to send it. The key to ensuring that your request is legally binding and respected is sending it via certified mail. This indicates that the collection agency got your demand letter, which may be vital if you need additional action.

Before sending, ensure to make multiple copies for your records. It's also a good idea to send copies to the original creditor and, in some cases, the Federal Trade Commission (FTC). This ensures that everyone is informed of the situation and that you proactively address potential violations.

It may seem like the last resort to send a demand letter, but what should you do if the communication continues? Let's explore your next steps.

The first step is to send the demand letter to prevent harassment from debt collectors. However, if the communication persists despite your request, you must take action to protect your rights. Here's what you should do:

Here is the decision tree outlining the steps, if communication continues after sending a demand letter. The flowchart guides you through the options available, from filing a complaint with the CFPB/FTC to seeking legal assistance and documenting communications.

Although the demand letter is effective, remember that if the debt collector ignores your rights, you must take additional action. Now that you understand how to handle continued contact, let's explore the limitations of a demand letter to help you set realistic expectations.

A demand letter can be a helpful tool for asserting your rights, but it's crucial to be aware of its limitations. Here are the key restrictions to keep in mind:

If you're facing challenges with debt collection, South East Client Services Inc. (SECS) specializes in offering flexible payment plans and online account management. They assist clients with debt recovery while providing a digital-first approach to ensure smooth communication.

Contact SECS Inc. for personalized assistance in managing your debt.

After addressing the limitations, let's quickly review why it's important to understand and utilize a demand letter to protect your rights regarding debt collection.

Understanding your rights under the Fair Debt Collection Practices Act (FDCPA) and how to use a demand letter effectively can help protect you from unfair and abusive debt collection practices. When dealing with debt collectors, you can take control of your situation and make sure you're treated fairly by following the steps listed.

South East Client Services Inc. (SECS) offers expert support in managing debt recovery with tailored solutions and a digital-first approach. Their expert team helps you to regain your control and reduce debt load.

If you're struggling with debt collection or need assistance managing your debt, contact SECS Inc. today for expert guidance and support.

This communication is from a debt collector. This is an attempt to collect a debt and any information obtained will be used for that purpose.

.jpg)